Our Investment Portfolio - June 2022

Investable assets, NOT including primary home, cars, collectibles, etc.

I wanted to walk through my portfolio briefly today as this will be the introduction to a larger part of what we do going forward.

Conjecture is great, but I like to put my money where my mouth is and actually follow through with what I’m doing and talk about my experiences.

Many newsletters only talk about theory and regurgitating what other people say.

My newsletter is based off of 20+ years of historical, political, and monetary study plus my experiences in investing.

I spent the first 10 years studying politics and history.

The last 10 years I have studied monetary, fiscal history and policy, along with investing through what I call our “family office.”

I am always a student. I am no expert. This is never financial advice, but only what I’m doing and what I see.

I hope to shortcut the process for you as to where I learn and what I’m doing and to track my record over time for posterity.

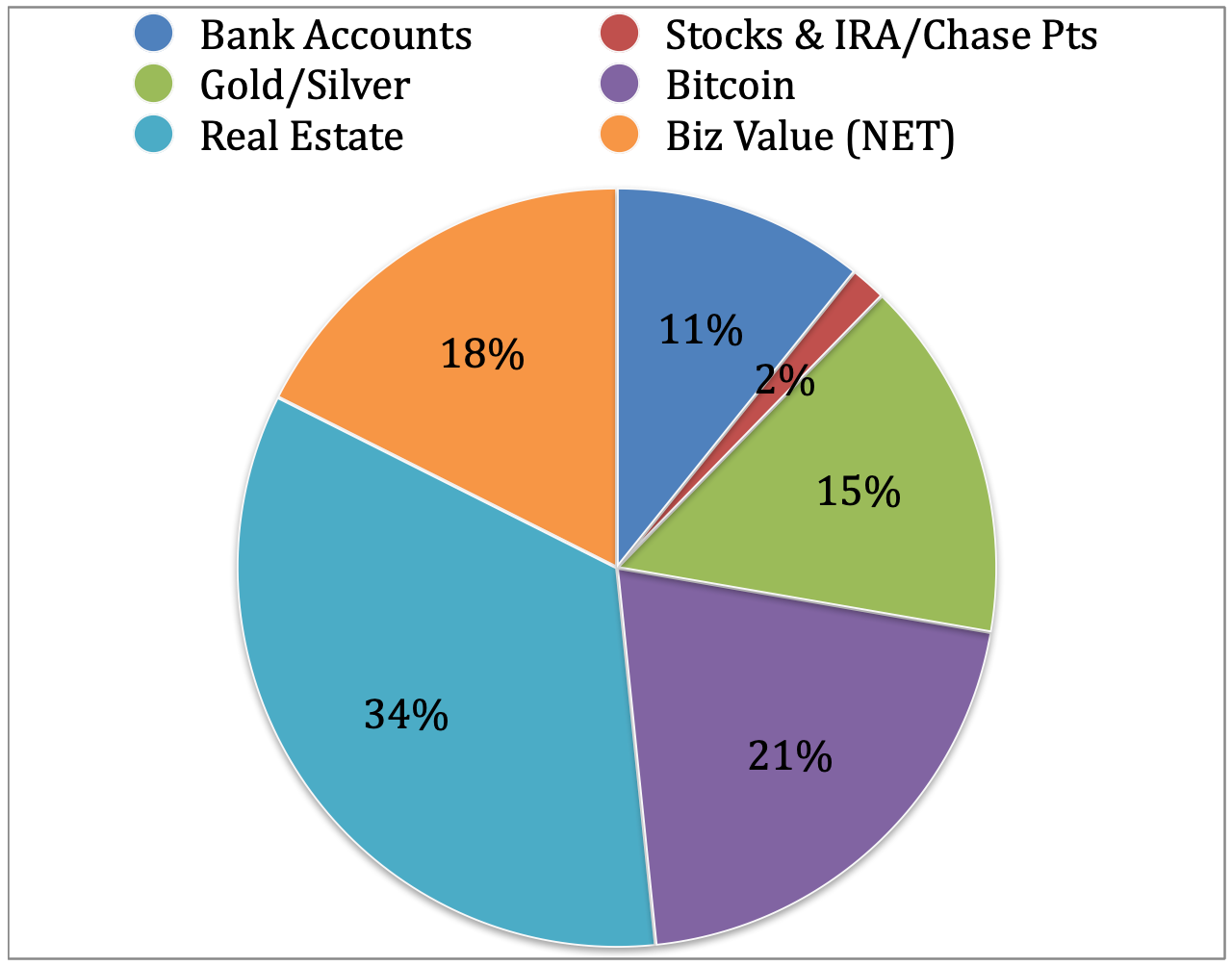

I will walk through the five main asset classes.

That being said here we go…

Real estate (positive cash flowing rental real estate)

If you can find a good deals in real estate and someone can rent it from you and you’re making positive cash flow that is awesome. That’s a really good short term and long term investment.

I have about 30-35% in rental real estate.

**Remember that the dollar is debt. There’s nothing backing it so the further you can get into good debt and buy appreciating assets you will win long-term as government continues devaluing the dollar. (ie. Refinancing real estate and pulling cash out tax-free to invest in other assets will be the people who win long-term. Savers get crushed by inflation and minuscule interest savings rates.)**

Bitcoin (digital assets)

If you are looking for something more long term….

My view on bitcoin is different than vast majority of people because I have gad the fortune of studying the network/asset for 100+ hours and see it very differently than the average investor.

It’s such a new asset that most people don’t understand it. I’m no expert but when the money aspect mixed with the political ramifications and opportunity for freedom it, just immediately clicked in my head about 2 years ago.

I believe it’s an incredible investment but it’s an even better freedom vehicle. Bitcoin is a longer time horizon like 5, 10, 20+ years where it looks like it will go to millions of dollars per coin.

The U.S. government looks at it as digital property or free-speech for that matter. It’s not stocks or securities. Many people think that crypto is all the same thing. There is Bitcoin, then there is everything else.

If you are looking for a long-term retirement and savings vehicle that will appreciate over time and keep your wealth safe and grow then bitcoin is where I have my bet placed.

I have about 20% or so in bitcoin.

**Before bitcoin was cut in half it was a lot greater percentage of my portfolio. I expect it to become majority of my portfolio again in the next few years as it increases in value.**

Gold and Silver (commodities; oil wells, uranium, copper, gold, silver, etc..)

I do have 15% in gold and silver also to diversify in the analog world.

This will hedge the chaos of the markets in the coming years.

Historically, gold and silver have maintained purchasing power and act as insurance for thousands of years.

True money, paper dollars are just claim checks on true money.

Paper (stocks and bonds)

I have a couple percent in gold stocks, my company’s stock, Jessica’s small IRA from a job 10 years ago, and credit card points.

Bonds are at a 5,000 year high because of how low the interest rates are, so I want none of that.

Stock market valuations, PE ratios, Buffett indicator, and every other technical/fundamental analysis you can run has the stock market overheated, so I have very little to nothing in paper assets.

There will be a time for stocks in “phase 2” once the defensive positions and hedges (insurance) pay out.

We will then sell those assets or lend against them and use that cash to buy businesses, cash flowing real estate, and dividend paying stocks (dividend aristocrats.)

Cash/Businesses

The other 30% I have is in cash personally and in the real estate business to operate daily.

I believe there will be more investments to buy on the cheap in the next 12-24 months.

This could also be cash or equity you have in businesses you own, private placements, limited or general partnerships.

Cash on hand is also good in case our long term view of inflation is wrong. If we experience massive deflation and the dollar increasing in strength, then we will be able to use the dry powder (cash) to buy many more assets.

I also have life insurance as well.

Conclusion

I am in a very defensive position and trying to be as liquid as possible and and have as much cash as possible on hand.

I don’t want a ton of cash on the balance sheet for more than 12 to 24 months because you are paying an option premium of real inflation which is around to 15-20% each year.

We have businesses to run and they require capital for employees, marketing, etc., which will grow as our investments grow and give us more capital to deploy in the business which will in turn grow more and throw off more cash flow.

Over the next decade, I believe bitcoin will be the “fastest horse” as they say.

Many of these assets will accrue value as the dollar dilutes and depreciates in value.

There will be a time to lend against those assets and purchase dividend paying stocks and more cash flowing real estate.

Stay tuned for “phase 2” in coming months/years when we transition in to more cash producing assets. I want to “dummy-proof” things and not be guessing if we are getting good deals.

Stay strong,

Brandon

Ps. We will continue watching the charts that show us when those assets are undervalued or overvalued compared to each other.

Tomorrow, we will talk briefly about how to value the markets and understand when to take action buying and selling.