Investment Portfolio Update - October 2022

Entering uncharted waters

(Listen to audio version of me reading👆)

Russell Brunson is one of my favorite business mentors in the world. He has taught me more about marketing, frameworks, and fundamentals than anyone I have ever studied.

He has a unique way of teaching and building frameworks.

The traditional financial advice and models that salespeople and Wall Street goons have been preaching for years have been blown apart. This year has been proof of that.

The 60/40 portfolio and just tossing your hard earned time and energy (wealth) in to someone’s hands who just siphon fees from you has shown to be a passable strategy when we are in a 40 year bond bull market.

Now that US debt tops $31 Trillion, entitlements are going bankrupt all within the next 10 years, inflation is through the roof, wars or protests breaking out around the world it can only lead you to ONE conclusion…

Time for understanding of true frameworks of how to live and invest in your life.

Most of us have been taught to operate in the derivatives world and not understand primary investments and proper frameworks to use.

I believe this is purposefully done so that when times get tough you have nowhere to run and stay in the arms of the rent-seekers.

The faster we can become independent and resilient the easier it is to be free and stay free and not feel dependent on the system.

I am always a student. I am no expert. This is never financial advice, but only what I’m doing and what I see.

Real estate (positive cash flowing rental real estate)

Looking to refinance one of our remaining rental properties that we own outright from using our HELOC to pay off another private money lender.

Looking to utilize a family member or friend who is looking to make more on the cash they have sitting in their bank than a couple pennies.

I would rather hold cash short term next 12 months and have long term debts at lowish rates paid off by our residents.

We have about ~35% in rental real estate.

**Remember that the dollar is debt. There’s nothing backing it so the further you can get into good debt and buy appreciating assets you will win long-term as government continues devaluing the dollar. (ie. Refinancing real estate and pulling cash out tax-free to invest in other assets will be the people who win long-term. Savers get crushed by inflation and minuscule interest savings rates.)**

Bitcoin

Still hovering around $20,000. I have continued putting big chunks of our cash in beyond my weekly DCA (dollar cost averaging) as it has dipped below $20,000.

The REAL power lies in the fact that when you own and custody bitcoin in your own cold storage hardware wallet, you have become your own sovereign bank. No one can freeze you out of the system or steal or dilute your wealth.

The world is getting crazier and each headline seemingly becomes a larger and larger billboards for bitcoin.

Bitcoin fixes so many of the monetary problems the central banks have brought on us, like inflation.

About ~20% in bitcoin.

**I expect bitcoin to become majority of my portfolio again in the next few years as it increases in value.**

Commodities (gold, silver, oil wells, uranium, copper, wheat, corn, etc..)

Commodities I believe will be in bull market over the next decade or two as derivatives crash and primary assets come front and center.

However, this will slowly get overtaken by bitcoin in the next few years. But I still want some analog in case we get hit by a meteor….

Again, I would rather diversify in the analog world spread around different vaults and geographic locations that we can access in emergency.

We have ~14% in gold/silver

Paper (stocks/bonds/IRA/etc.)

I have a couple percent in my company’s stock (I have stopped contributing here), and credit card points, Jessica’s small IRA was in cash/short term bonds and I took it all and bought the Grayscale Bitcoin Trust (GBTC) with a limit order and got it at super low prices.

#GBTC is NOT bitcoin. It is a paper derivative of that and it’s a leveraged play on bitcoin that I don’t plan on touching.

Still not keen on things I cannot control. Been thinking about stocks a little bit but I do think you could see another leg down still on blue chip dividend paying stocks.

Again, there will be a time for stocks in “phase 2” once the defensive positions and hedges (insurance) pay out.

We will then sell those assets or lend against them and use that cash to buy businesses, cash flowing apartments/storage/mobile home parks, and dividend paying stocks (dividend aristocrats.)

We have ~2% in stocks

Cash/Businesses

I still believe there will be more investments to buy on the cheap in the next 12 months or so.

This could also be cash or equity you have in businesses you own, private placements, limited or general partnerships.

Cash on hand is also good in case our long term view of inflation is wrong. If we experience massive deflation and the dollar increasing in strength, then we will be able to use the dry powder (cash) to buy many more assets.

I also have life insurance as well that I may roll in to whole life cash value at some point. Going to be talking to Ron Sneller about that at some point in the future and the pros and cons of that move.

Expect to have more cash in the next month here as we refinance that rental. Then I would feel very comfortable going in to Q4 and Q1 2023.

~29% is in cash.

Conclusion

Bonds prices and equities are not supposed to go down at the same time.

That is exactly what have seen this year. ALL assets classes going down.

Oil has come back down to break even on the year.

What an insane time. “Demand destruction” is real.

This is why I have been a big proponent over the past few months of sitting on more dry powder (cash.)

Soon as we get this refinance done and have cash back in the hopper we will sit tight for a quarter or two.

Until we see what is really happening here it will be harder to deploy capital until we are really heading up from a true bottom.

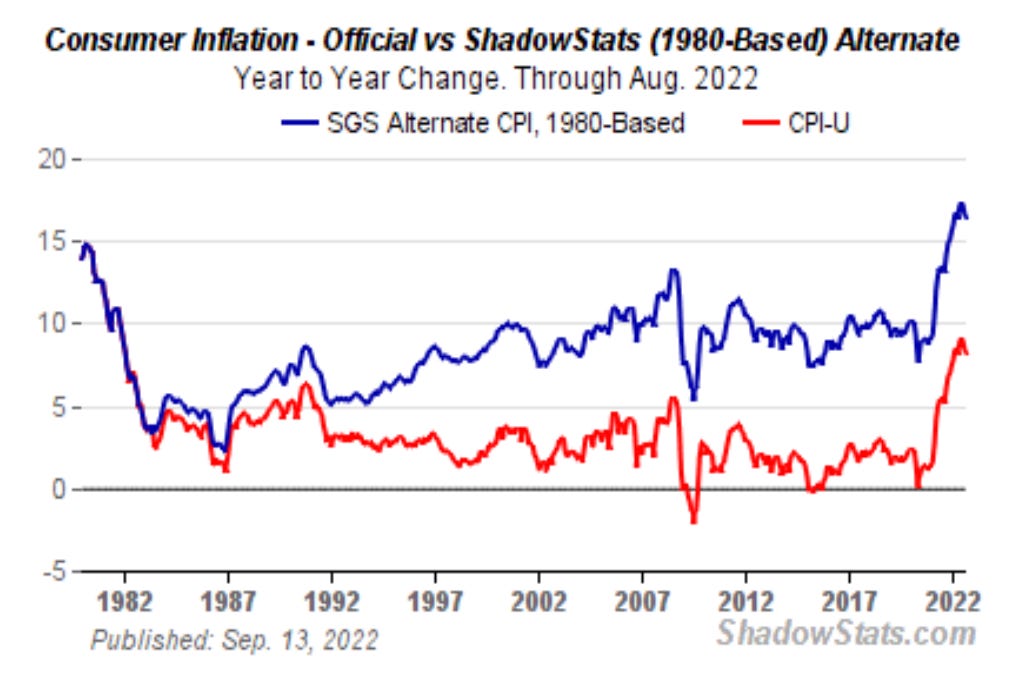

Trying to stay very liquid and don’t want a ton of cash on the balance sheet for more than about 12 more months because you are paying an option premium of REAL inflation which is around to 15-20% each year.

Keep in mind when making an investment it has to be beating 20-24% each year as Warren Buffett says.

Why I love saving IN bitcoin instead of US dollars, because it grows CAGR (compound annual growth rate) at 100-150%/year.

Stay strong,

Brandon

My newsletter is based off of 20+ years of historical, political, and monetary study plus my experiences in investing.

I spent the first 10 years studying politics and history.

The last 10 years I have studied monetary, fiscal history and policy, along with investing through what I call our “family office.”

I always mention to anyone that will listen: you must know the financial and money games for ANY of the political side to make any sense.

***Special tip: watch the credit market (bonds) especially the 10 year to see where the markets are going to go. That tells us where the stock and rest of markets will go.